My 2022 forecast sales range is slightly lower than what I was looking for last year; it’s between 5.74 million and 6.16 million. The recent existing-home sales data at 6.5 million surprised me so much that I believe some of the December closings fell into January, and if you take the two-month average, it looks a bit more like the trend sales data we saw toward the end of 2021.

Make no mistake, existing home sales have been outperforming my estimates, with a few sales prints over 6.2 million as mortgage buyers became more active toward the end of the year, which breaks from the seasonal patterns.

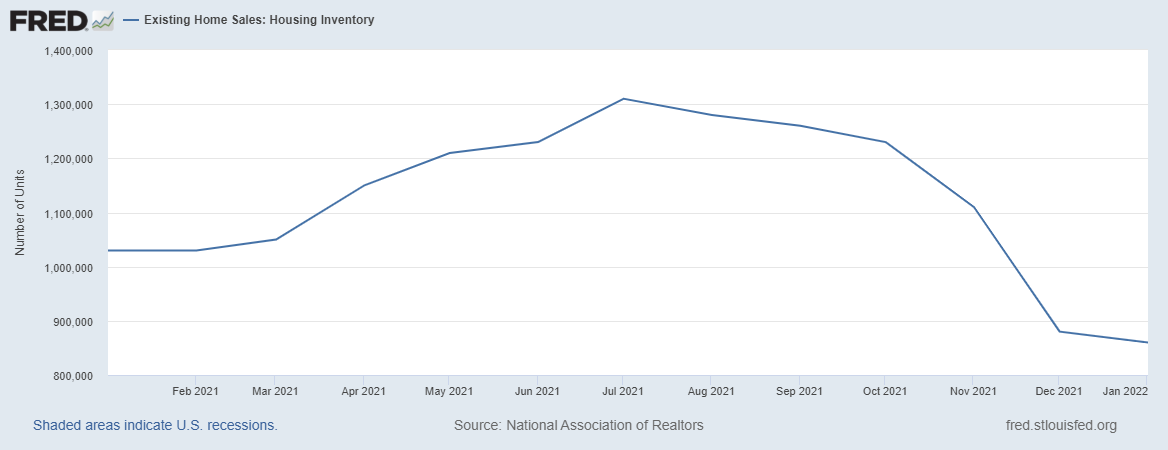

As you can see above, existing home sales had a nice fall and winter, which shouldn’t be surprising. Our best sales data have come in the fall and winter the last two years and even in the previous expansion.

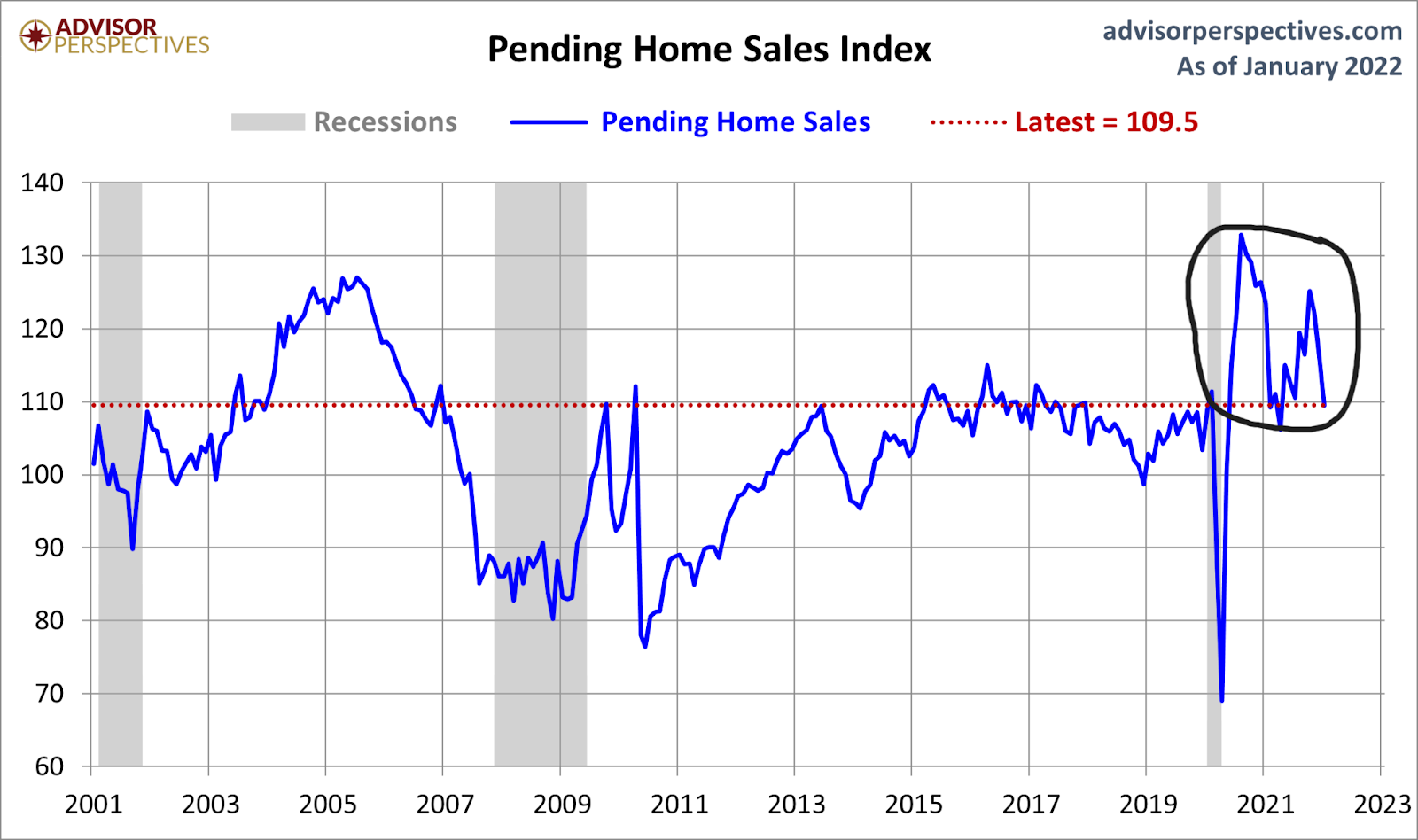

2022 Pending home sales

Now looking ahead, the recent pending home sales data look about right to me after an outperforming second half of 2021. Unlike the surge in make-up demand we saw at the end of 2020, this recent outperforming data should moderate just due to traditional demand limits with the housing market at record low inventory levels. The question is, where do we find the sales base in 2022 to work from?

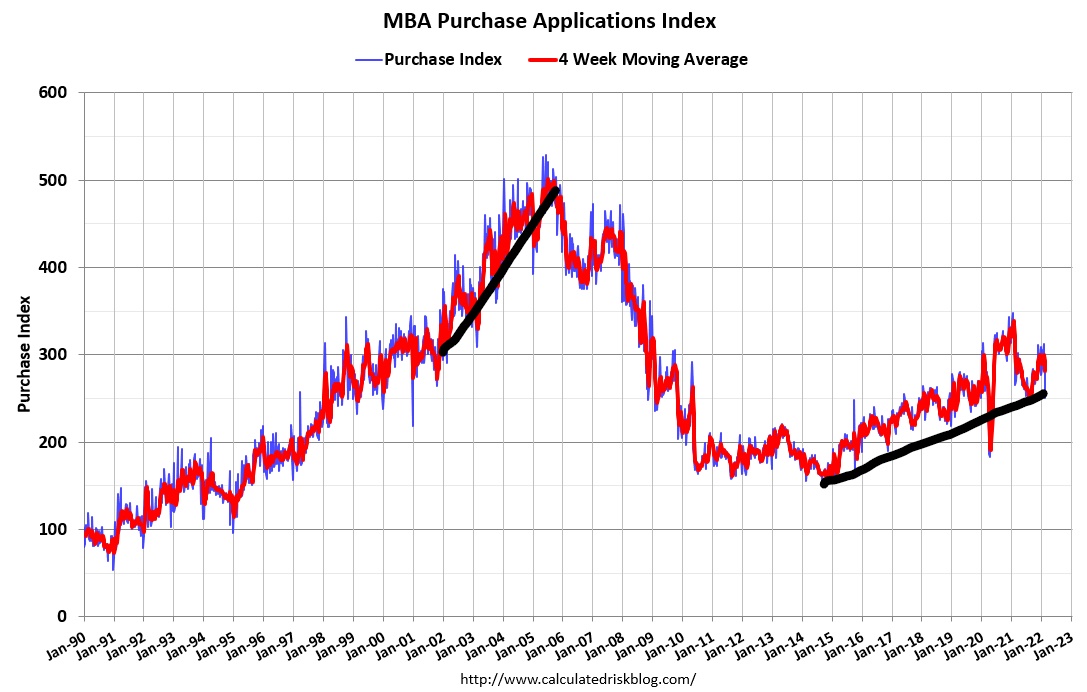

Last year we had a few sales print above 6.2 million, so I anticipated a few prints under 5.84 million. We only got one print. That was a big clue that housing was doing much better than I thought. This year, we should see a print or two below 5.74 million. However, if the sales trend is between 5.74 million and 6.16 million, demand is stable. So far this year, this is what I see in the purchase application data as well.

Even if I make COVID-19 adjustments, demand is only stable and not growing. Remember, with the MBA purchase application data, it’s very seasonal — volumes typically fall after May. Last year and the year before, we saw growth in this data line in the second half of the year, which isn’t normally the trend. We might need to keep an eye on this later in the year.

However, I genuinely believe that all the COVID-19 adjustments I have made with this data line don’t need to happen anymore. We can be more mindful that the year-over-year data aren’t working from the surge in make-up demand we saw in 2020 and spilling into the first two months of 2021.

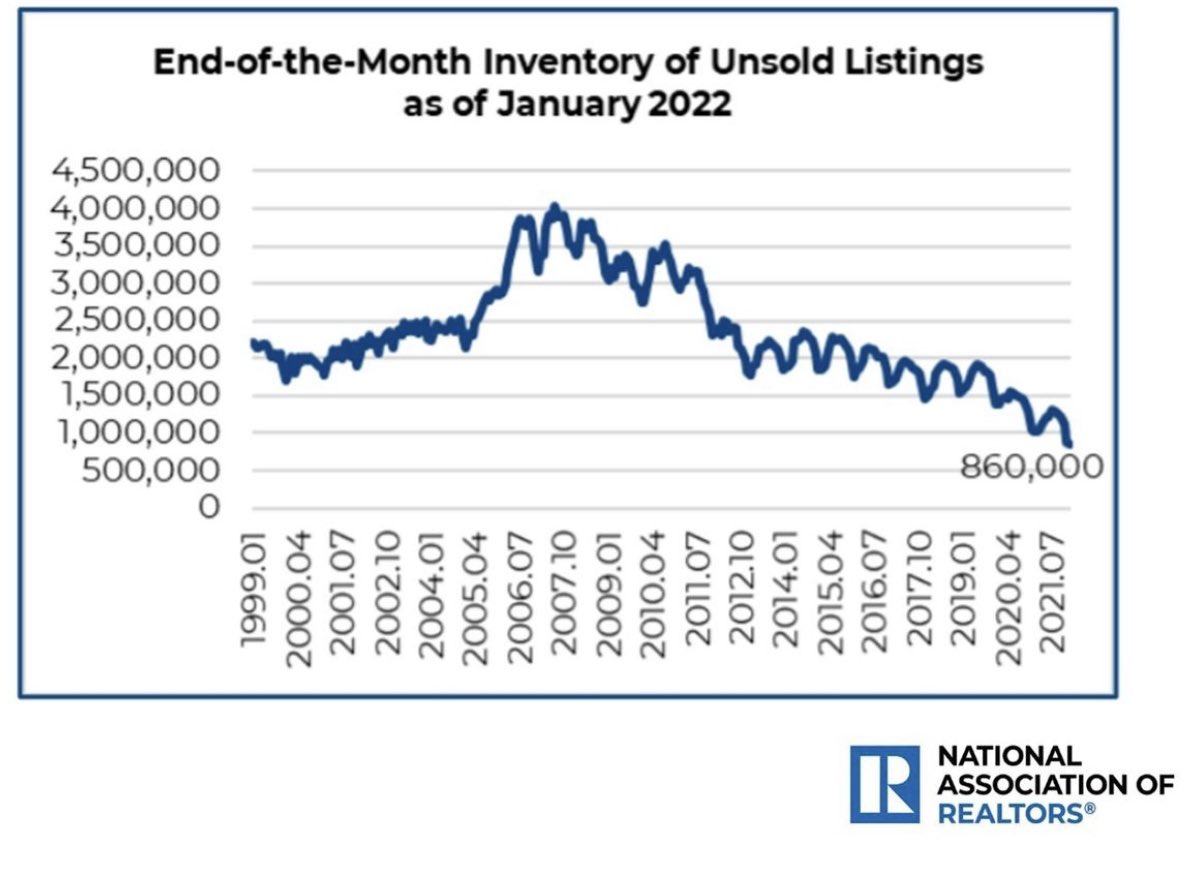

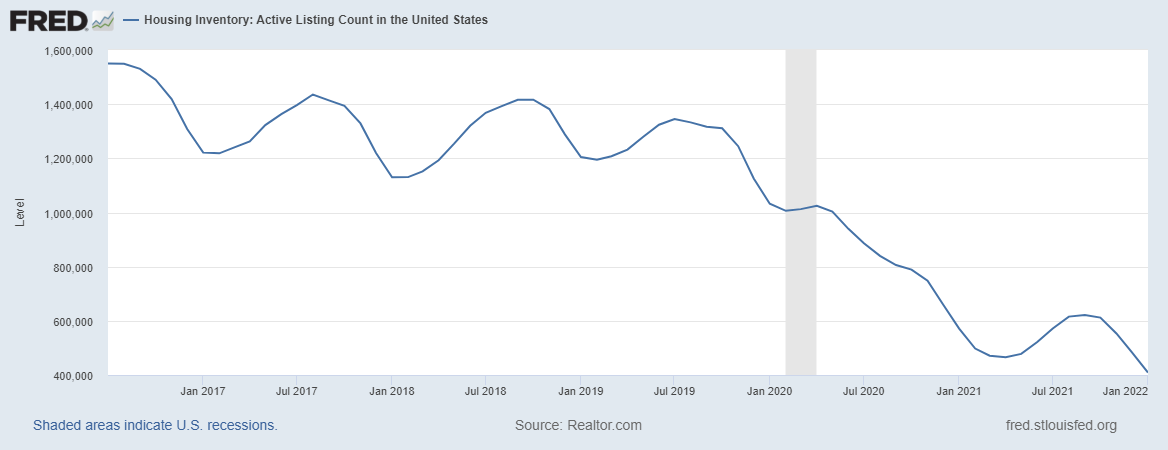

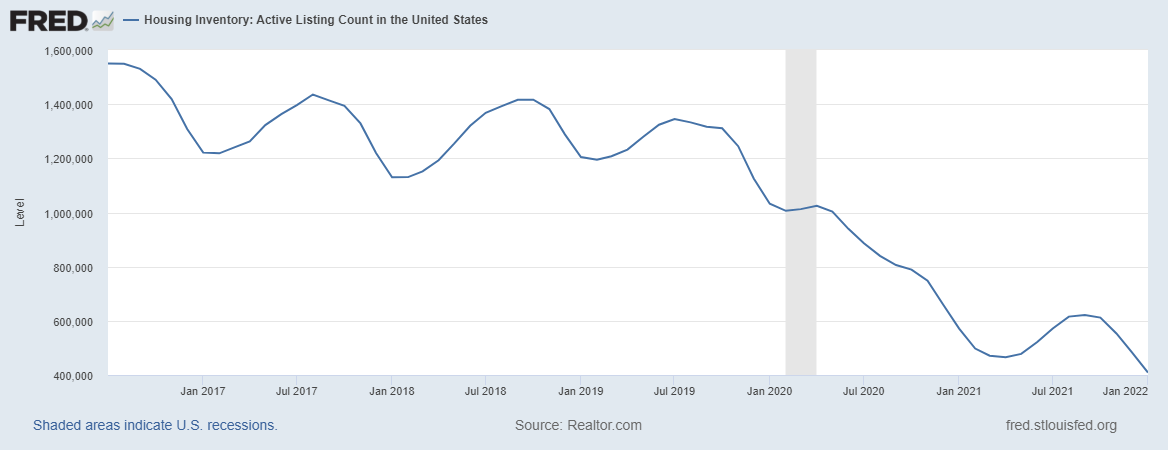

Of course, the main issue we have in the U.S. housing market is the inventory crisis, as we have started 2022 with fresh new all-time lows in inventory. Inventory is always very seasonal, and we should see the total inventory increase in the upcoming months. If this doesn’t happen in a meaningful way, we might have to think of creative ways to create more inventory. I hope higher mortgage rates do their thing and make more days on the market than in the past.

I hope that the seasonal inventory push will happen again in 2022 and that higher mortgage rates will create more days on the market so that we don’t start 2023 at fresh new all-time lows. This is critical. The U.S. has lagged a lot of countries over the year in home price growth, and my fear for 2020-2024 has always been that we would see five years of unhealthy home price growth. So far, this fear is playing out.

Active inventory listings are at crisis levels, pushing home prices well beyond my five-year cumulative home-price growth level in just two years.

It has been tricky trying to find proper trends in housing data after COVID-19 made some of the year-over-year data too extreme to take seriously. However, starting in March, I believe that the purchase application data will be back to normal, and the April reporting of March housing data will be more in line with traditional housing data.

The rule of thumb for the rest of the year is that if existing home sales get above 6.16 million, you should view that as a beat, while if they’re trending below 5.74 million with several prints under that level, then we have housing softness. The upside of that housing softness, if it occurs, is that it should create more days on the market and give this housing sector a much-needed breather. As I have stressed time and time again, this is a very unhealthy housing market due to a lack of inventory in a time when the most prominent housing demographic patch ever recorded in history needs to find shelter.

Despite 3-month slump, pending home sales look just right - HousingWire

Read More

No comments:

Post a Comment